Though spatial computing and all its subsegments continue to hold great potential, they also face headwinds. Factors holding them back include challenged technological advancement and cultural adoption. However, bright spots include the rise of AI-powered smart glasses.

For example, as seen in Meta’s earnings, smart glasses have offset declines in other subsegments, such as consumer VR. Altogether, it’s a mixed story with both positive and negative drivers. The good news is that the positives will mostly outweigh the negatives in the near term.

To wrap some numbers around these claims, spatial revenue is projected to grow from $28.5 billion in 2025 to $61.4 billion in 2030. That’s steep growth, driven by a projected inflection next year as new smart glasses blitz the market from Apple, Meta, Google (AndroidXR), and others.

What else is driving revenues, and what are strategic implications? These questions are tackled in the latest spatial revenue forecast from our research arm, ARtillery Intelligence. This Behind the Numbers series excerpts insights, continuing here with consumer spending estimates.

https://artilleryiq.com/reports/spatial-computing-revenue-forecast-q1-2026/

Numbers Game

After the last installment of this series looked at XR device unit sales projections, we move on to consumer spending. Including both hardware and software, how much are consumers spending on XR today. More importantly, how is that projected to grow over the next five years?

Starting at the top, global XR consumer spending is projected to grow from U.S. $6.86 billion in 2025 to U.S. $27.62 billion in 2030. This is rapid growth, so what’s driving it? It’s primarily all about the popularity, momentum, and escalating tech-giant investment in AI-driven smart glasses.

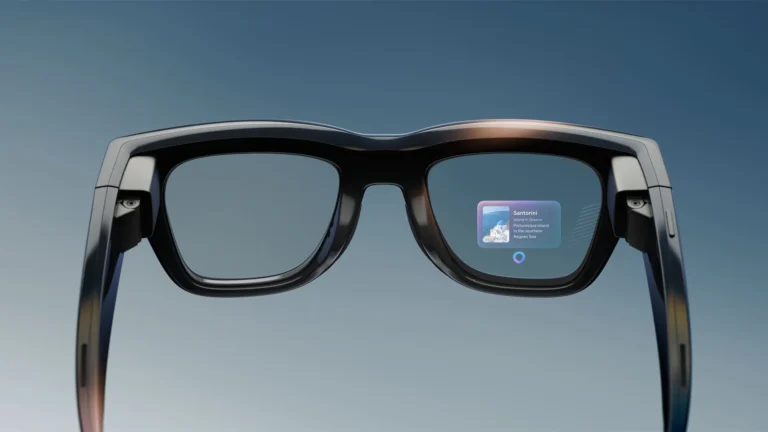

Going deeper on that last point, the market for low-immersion smart glasses is heating up. This is driven by the market demand that Ray-Ban Meta Smartglasses (RMS) have validated. That success emboldened Meta to double down with Meta Ray-Ban Display Glasses (MRD).

But it’s not just about Meta. The same demand signals attract others to the land grab. For example, Google has been frenetic in its XR strategies over the past decade. But with RMS’ market validation, Google’s Android XR platform now focuses on supporting smart glasses.

Purpose Built

Synthesizing all the above, when we say low-immersion smart glasses, it includes non-display and flat-AR display glasses (see our XR device definitions and segmentation). These and other points on the spatial spectrum are diverging and diversifying into purpose-built hardware.

The short version is that non-display and flat-AR display glasses are characterized by toned-down visuals – or even no visuals at all – which enable sleeker and more stylish hardware, as well as lower price tags. This has stimulated consumer demand, to the tune of 10-million+ lifetime units sold.

Zeroing in on flat-AR, the category is subdivided by utility display glasses and video display glasses. The former is represented by Meta Ray-Ban Display glasses, as well as devices like Even Realities G2. They offer simple displays for utilities like messaging and navigation.

Video display glasses conversely offer private virtual screens for gaming and entertainment. Players like VITURE offer simple yet robust experiences that are framed in the activities that consumers already know, and the content they already own. No learning curve needed.

Driving Force

Meanwhile, the driving force for much of the above – especially non-display and utility display glasses – continues to be AI. Previously deemed underwhelming, flat-AR and ‘audio AR’ gain value and utility when positioned as intelligent and ambient assistants that annotate the world.

They breed smarter situational awareness for wearers. This represents a design shift that prioritizes contextual intelligence over immersive visuals and holography. But, don’t count out the latter – especially Snap’s forthcoming consumer spectacles launching later this year.

Of course, all of the above doesn’t tell the full story for consumer XR spending…though it is where the momentum lies. Consumer VR adoption is another piece of the pie. However, growth is decelerating as VR reaches a saturation point, relative to its current demand ceiling.

Fortunately for Meta, it has diversified its XR mix, so all the above growth in smart glasses offsets declines in VR. Similar can be said for the Android XR platform, whose form-factor diversification is baked in. Others will follow suit, such as Apple’s rumored shifts towards smart glasses.

We’ll pause there and circle back in the next Behind the Numbers installment with more numbers & narratives. Meanwhile, check out the full report.